Identifying and Developing European CCS Hubs

Key messages

A low carbon EU should be inclusive with a comprehensive collection network enabling emitters large and small to connect to CO₂ storage and create value in the Net Zero economy.

Developing such CO₂ gathering networks & clusters linked to CO₂ storage hubs via trunk pipeline networks and shipping routes is the lowest cost route to creating low carbon sustainable growth.

The EU has a number of large CO₂ emission clusters, plus it benefits from world class CO₂ storage formations. Connecting emissions clusters to the storage formations will often cross national boundaries – a regional collaborative approach incorporating adjacent member states is therefore needed.

A necessity for the creation of hubs and clusters, is policy supported by suitable (financial) instruments that can facilitate deployment. However, an often overlooked fact is that, in addition to policy instruments, the maturation of hubs and clusters requires dedicated people to tailor and plan deployment. Only with both dedicated people and policies can CCS be deployed to accelerate the transformation to Net Zero industrial and power generation clusters.

Efficient and effective design and delivery of optimal hubs and clusters requires regional development organisations, each drawn from relevant Member States, working with national market makers and transport & storage network developers.

Scope and limitations of this report

ZEP was requested, by the EU Commission, to enlarge on the potential core areas for near-term European CCS deployment that had been identified in their earlier report An Executable Plan for enabling CCS in Europe. This short note expands on the contribution toward Net Zero and a sustainable Europe that deployment of CCS hubs and clusters can deliver.

In creating this report it was found that only limited data could be obtained for some of the regions that have been identified as geographically advantaged.

Upon investigation it was noted that only those regions which had developed local delivery organisations were in a position to deliver the bottom-up analyses required to underpin informed investment decisions in CO₂ infrastructure. It was also found that many of these organisations are at risk as they depend on local or short term funding yet the development of hubs and clusters requires a multi-decade approach to pan-European development similar to the approach adopted in the Connecting Europe Facility.

Owing to the lack of data it has only been possible to outline some regions and this document is therefore being issued with the expectation of revision should more information become available.

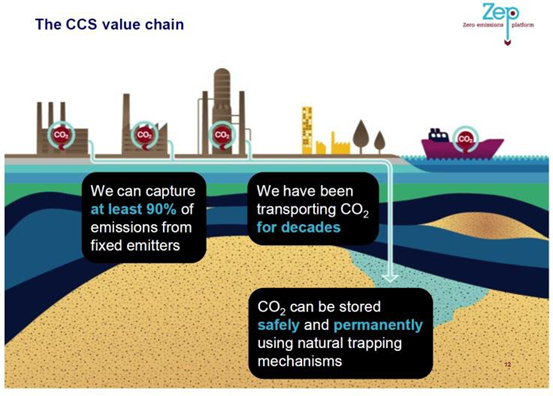

CCS can deliver rapid large scale reductions in CO2 emissions

The COP21 agreement from Paris in 2015 has made it abundantly clear that CO2 has to be collected and disposed of, not just released into the environment.

The only large scale permanent disposal route for CO2 is to re- inject it into deep rock formations. This disposal route is proven: in Europe the Norwegian company Statoil has almost 20 years of CO2 storage experience; in the USA large scale injection for CO2 EOR started in the 80s; while the technology applied has many elements in common to those used in the production and storage of oil and gas.

CCS has the ability to deliver to EU Member States the rapid reductions in CO2 emissions required to support INDCs while, at the same time, having minimal impact on current infrastructure. A capture equipped energy, waste incineration or manufacturing plant has only a slightly larger footprint than the original plant, while CO2 transport pipelines, like natural gas, chemical and oil product pipelines, are buried. The CCS system fits comfortably alongside existing power generation, power transport and manufacturing infrastructure, and unobtrusively delivers huge multi-million tonne reductions in CO2 emissions.

Why emissions clusters and storage hubs?

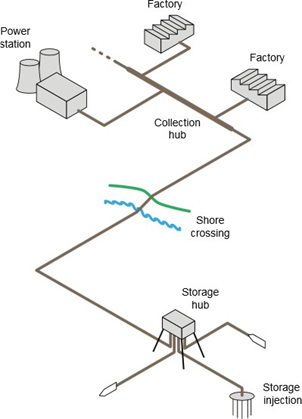

Storage requires suitable geological strata, but these do not exist under every EU region therefore CO2 transport is required. This is analogous to natural gas transportation where pipelines cross the continent linking gas fields to customers.

The transport and injection of CO2, like that of natural gas, benefits from economies of scale – it is more cost effective to build one large trunk pipeline than to build three smaller pipelines. The same holds for injection infrastructure and aquifer storage monitoringtechnology. A schematic representation is depicted on the right1.

Large emission sources also tend to be clustered – because they often historically grew near coal fields, ports or rivers; and because there are benefits to clustering manufacturing near to refining and power generation.

This leads logically to the development of CO2 collection clusters, trunk transmission networks, and CO2 storage hubs. Once established a hub and cluster network can significantly reduce the cost of entry to new decarbonised companies. Industrial clusters represent a real opportunity to exploit shared infrastructure that many parties can use, therefore benefiting and reducing cost for multiple (and especially smaller) emitters. Strategically sized transport & storage infrastructure built with additional/spare capacity allows the investment decision to be de-risked for the emitter, allowing for potentially more attractive capital structures and funding approaches, which would reduce risk and cost for many potential low carbon projects. Shared infrastructure with sufficient, proved storage capacity also allows emitters to separate their investment decisions (in terms of both time and technology) from the development of the network. This is important to maximmaximise deployment and exploitation of CCS and realise benefits of scale2.

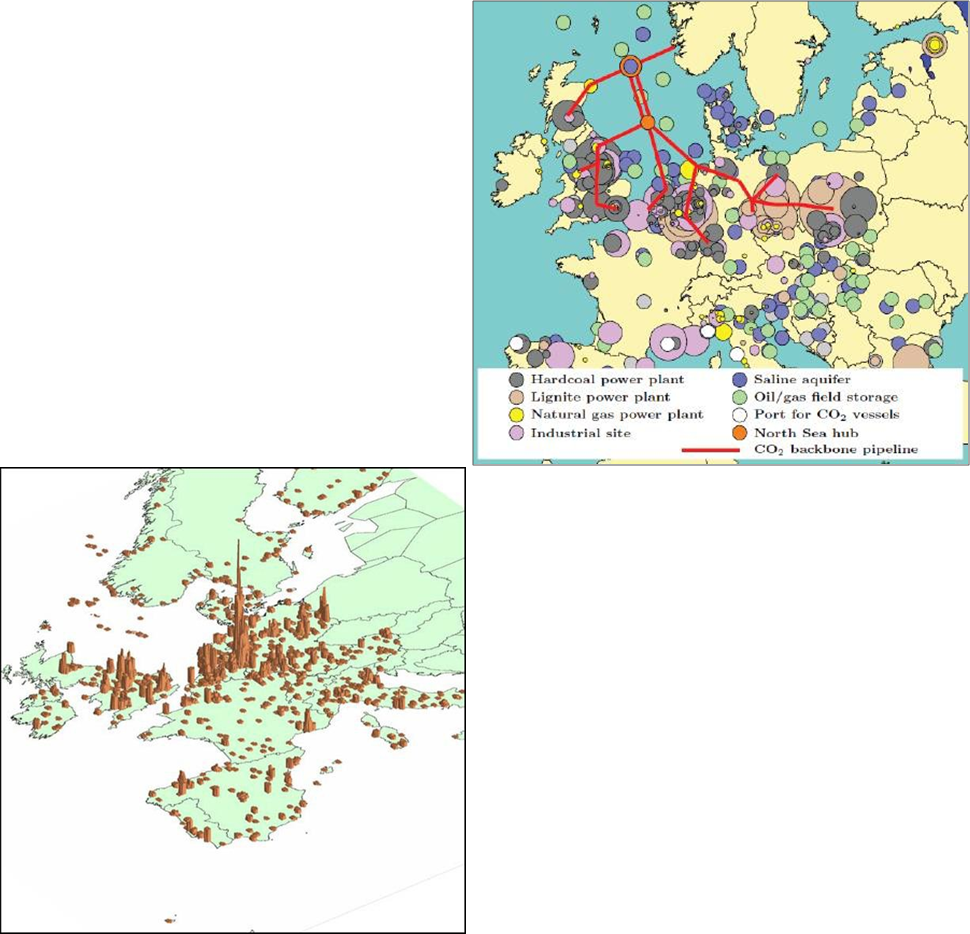

Europe’s advantaged global position

The EU is lucky to have a world class storage region – the North Sea basin. This basin has many tens of billions of tonnes (Gt) of CO2 storage capacity and has the advantage of being offshore thereby reducing the public acceptance barrier. Offshore development, however, has a higher capital cost than onshore and benefits even more from the cost savings delivered by economies of scale. The Baltic Sea has also been recently evaluated and significant storage resources in the multi-Gt range have been identified.

Onshore CO2 storage will also be important and is already proven in Canada and in the USA. Recent experience in the EU indicates that public acceptance is more challenging to obtain than in the USA and Canada, due substantially to population concentration and location, therefore it is likely that offshore storage will precede onshore storage. There might, however, be exceptions to this especially in Eastern Europe where there is an existing onshore CO2 EOR industry.

Many of Europe’s largest carbon emitters (both power plants and industrial facilities) are already ‘clustered’ together around major ports such as Rotterdam, Duisburg, Hamburg, Humberside, Teesside, Grangemouth, Antwerp, Le Havre and Merseyside.

Importantly, some industrial clusters are also close to excellent and extensive geological CO2 storage opportunities. For example on the North Sea coast of the UK, the Teesside area’s industry represents 5.6 per cent of the UK’s industrial emissions, while the Yorkshire and Humber region represents 10 percent of total UK CO2 emissions.3,4

EU Emissions clusters, from (left) IEAGHG5 and (right) ZEP6 Carbon Capture and Storage in Energy-intensive Industries

How are hubs and clusters encouraged to develop?

The challenge with CCS is scale. Full scale CCS projects can make a massive impact on the CO2 emission reductions targets of a member state – a single commercial scale project will remove between 1Mtpa and 5Mtpa. For reference 1Mtpa is equivalent to removing the emissions of about 250,000 EU cars. However, the large scale of a CCS project – which delivers a large emission reduction – means that the individual project capital cost is significant, commonly over €1Bln. In order to fund this level of investment, finance is generally sought over a period of up to 25 years – this exposes projects to significant counterparty risk as described in ZEP’s T&S business model report, and also to political/policy risk. While the renewable industry, which also faces the need for significant capital investment, has overcome this challenge through the use of policy led stimuli like subsidy, feed in tariffs and loan guarantees this bridge has not evolved yet for CCS industry.

CCS is an emissions control technology, in order avoid damages and resulting cost to the environment and society. This helps explain why CCS has not managed to develop an effective funding model as it is an adjunct to existing processes (coal/gas power generation + capture; manufacturing + capture) rather than an industry in its own right (wind generation, solar generation). Another challenge is that transport infrastructure needs to be developed to link CO2 emitters to CO2 storage sites from scratch. By contrast renewable generation benefits from the Member State transmission grids. The capital risk for grid upgrades can often be borne by regulated utilities not by an individual renewable energy project. For this reason ZEP is recommending the disaggregation of the CCS chain – the separation of capture from transport and storage infrastructure development.

This separation requires the development of key transport infrastructure, sized correctly for regional requirements. Some of the infrastructure can take advantage of the flexibility of ship transport – requiring the provision of liquefaction, loading and offloading facilities rather than whole pipeline systems. It also requires the development of strategic storage hubs.

In order for a region to be ready for the development of CCS a number of critical success factors need to be in place. These are described in full in ZEP’s Executable Plan, but the key ones that are being selected here in order to identify potential hubs and clusters are:

- Ambition to decarbonise industry and energy

- The presence of emissions sources and storage formations

- A politically supportive industrial region and member state

- The potential for EU regional funding

- The potential for economic value creation and retention through the development of CO2 advantaged manufacturing of products or CO2 utilisation opportunities.

A necessity for the creation of hubs and clusters is a policy supported by suitable (financial) instruments that can facilitate such development. Effective delivery requires coordination by regional development organisations, each drawn from relevant Member States, working with national market makers and T&S network developers.

In the absence of regional development organisations ZEP has drawn upon the knowledge of its members to create outline development plans for a number of candidate regions. The fact that the level of detail of the summary plans varies highlights the need for the key first step of stimulating the creation of these regional organisations. Thanks must be given to those organisations that do exist and who have helped: Gassnova; Scottish Carbon Capture & Storage (SCCS); the CCSA; the Rotterdam Climate Initiative and the GCCSI.

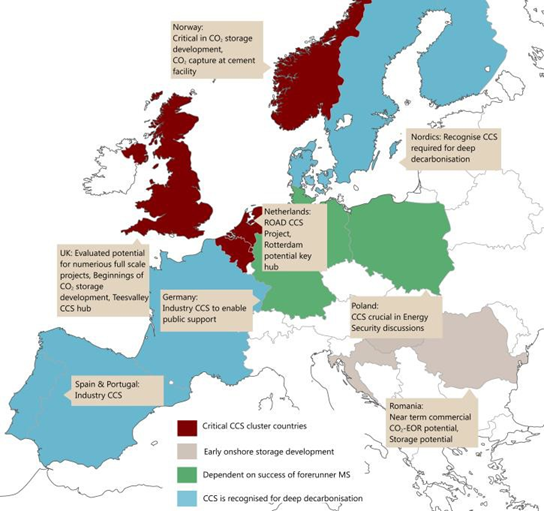

The figure above shows the candidate regions that have been identified as possessing many of the key characteristics: CO2 sources, sinks, and political awareness of the opportunity presented by CCS.

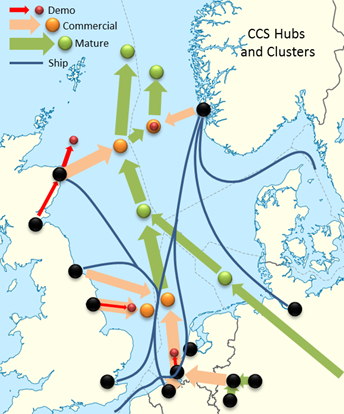

Potential regional groupings of emissions clusters and hubs

The lack of identified regional development organisations or proxies thereof in Poland, Germany, Romania and Spain/Portugal means that ZEP has to date been unable to mature notional CCS development options for these key regions.

A critical recommendation is therefore to request that the Commission work with these regions to establish organisations that can effectively outline the opportunities for rapid and deep carbon reduction by CCS.

The figure above outlines a potential integrated development opportunity for the countries that skirt the North Sea. It is possible to start small with demonstration scale projects (1-3 Mtpa), then develop initial commercial scale cross border connections, and finally install the full scale (mature) interconnection trunk lines. Ship transport is ever present connecting smaller sources to the established storage hubs, initially transporting CO2 between onshore hubs until offshore unloading has been developed.

The four initial components are: Rotterdam hub; the UK Southern North Sea hub; the UK Scottish hub; and the Scandinavia hub. These regions would also benefit from formal regional development organisations.

The nature of a regional development organisation

A regional development organisation is envisaged by ZEP as a small body with established full time staff.

- The staff would be drawn from the member states represented in the regional organisation and would have strong links back to the relevant ministries.

- Staff competence would cover capture, power and industry, transport, geological storage, public engagement, economics, energy system modelling, business & finance, R&D, climate science, regulatory and policy.

- The mandate would be to

- Map and understand the nature and longevity of emission sources – working closely with companies and local stakeholders

- Develop policy recommendations that would lead to the capture of these emission sources, and use these data to create forecasts of captured CO2, while also ensuring that these forecasts are linked to the INDCs and incorporated in system modelling tools such as the UK ESME model7.

- Identify potential CO2 stores (EOR, depleted field, and saline formation) and develop maturation plans

- Identify transport corridors and perform initial impact assessments

- Develop the best local business models (point-to-point, market maker) for delivery of CO2 capture, transport and storage within the region

- Work together with regional and EU policy makers to deliver the CO2 emission reduction potential of CCS – building this into the (I)NDCs.

A coordination mechanism between regional organisations will be important and could potentially leverage the already existing EU (EEPR) projects network, or could be facilitated by an ETIP such as ZEP.

Descriptions of some of the potential hubs and clusters

As mentioned in the earlier sections not all key regions can be described owing to a lack of integrated data. The following sections outline the hubs and clusters for which some data exists.

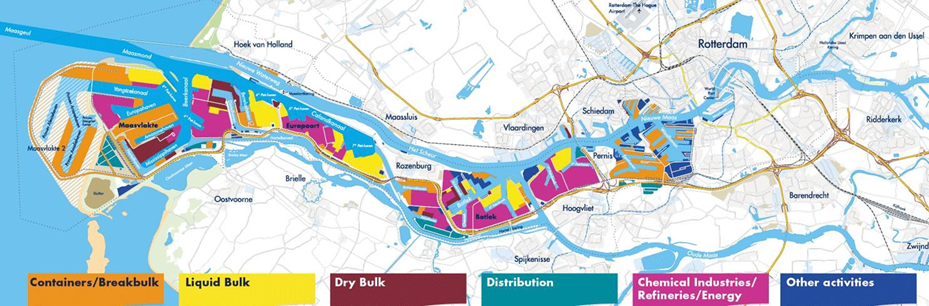

The Rotterdam CO2 hub

The port of Rotterdam industrial complex emitted about 30Mt CO2 in 20148. It is by far the largest port in the EU, and is also located near to the second largest port Antwerp. The port is the terminus of existing pipeline corridors to Antwerp, and the Rhein and Ruhr industrialised regions, and naturally is well suited to CO2 ship and barge transport.

The region pioneered the use of waste CO2 with the development of OCAP9 in 2003. They are host to the ROAD10 CCS project which is in receipt of EEPR11 funding.

The ROAD project has identified a cluster of depleted gas fields, the Rijn oil field and a saline aquifer all operated by TAQA. The fields represent the low cost kick start for CCS in Europe, and one field is already in receipt of the first ever EU storage permit.

The map above indicates sources and potential pipeline and ship transport routes.

There is an opportunity to extend the Rotterdam hub into a regional “Target Zero emission” cluster. The current team is composed of part time members from some of the stakeholder companies in the port.

The team has identified a number of Projects of Common Interest that can either increase the capacity of flow by building infrastructure that crosses a border or increase the capacity of flow as a result of construction in a single country. Eligible projects could be:

- A pipeline between Antwerp and Rotterdam

- A pipeline between Duisburg and Rotterdam

- A CO2 gathering system in Antwerp, Duisburg, Le Havre, Hamburg or Rotterdam

- Buffer storage and loading/unloading facilities at Antwerp, Duisburg, Le Havre, Hamburg or Rotterdam

- A pipeline network to the first few offshore storage locations, (excluding injection infrastructure on platforms, which is not eligible).

At present the whole potential for a carbon capture hub hinges on the success of the ROAD project. The development of a multi-country regional deployment organisation here could greatly improve the potential to deliver rapid and deep CO2 emission cuts in at least three member states.

UK hubs

Until recently a lot of work has been done in the UK in trying to develop up to two potential end-to-end CCS projects. These projects could have stimulated the development of CCS hubs in the North and the South of the UK – and such follow on projects like the Teeside Collective industrial cluster were in development.

The project funding was removed by the member state at the end of 2015, however, the study work did serve to outline that there was potential to create effective hubs and clusters in this region.

The work is presented on the following pages, with the caveat there is a significant risk that the UK potential will be lost if an effective regional development organisation is not established that can continue the work done by the two now disbanded major projects.

UK Southern North Sea CCS hub

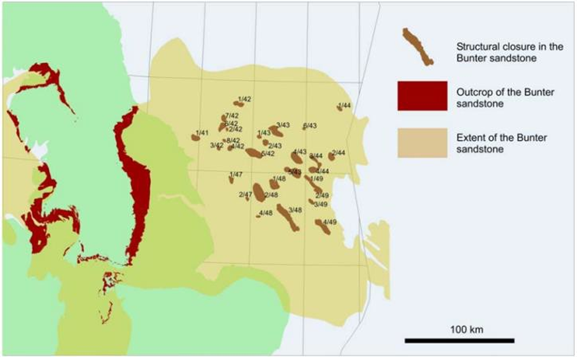

There is significant potential to develop a CCS hub in the Southern North Sea (SNS) based around the ‘Endurance’12 storage site, which lies within the Bunter sandstone formation in the UK Continental Shelf.

The Endurance store has recently been appraised for use with the UK White Rose CCS project. As such it has de- risked the Bunter as a storage formation. The wider Bunter Sandstone could offer CO2 storage opportunities in excess of 3 Gt CO 13.

The SNS hub offers CCS opportunities for a range of regions with substantial CO2 emissions, including both the Teesside and Yorkshire-Humber regions. The potential also exists to transport CO2 from continental Europe, including from the Rotterdam region, by either pipeline or ship.

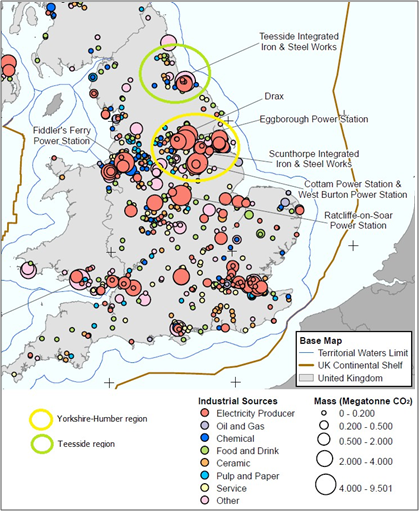

Southern UK emissions sources (2013)14 are shown on the right. The Yorkshire-Humber and Teesside regions combined emit more than 70 MtCO2 per year, equivalent to 15% of total UK industrial emissions.

Industrial emissions from Yorkshire-Humber alone are estimated at more than 50 Mt per annum from a region that employed more than 280,000 people in manufacturing industries in 201415. In addition, the Tees Valley Process Industry Cluster is one of the largest in the UK, covering a diverse sector base of chemicals, petrochemicals, steel and energy companies. The cluster employs c. 20,000 people, has a GDP of c. £10bn and exports of c. £4bn per annum16.

The Teesside Collective – an example of a nascent regional development organisation

In recent years local stakeholders have joined forces in the Teesside area of Northern England (see map on previous page) in the UK. The formation of the group was spurred on by the UK CCS commercialisation efforts, but then was underpinned by some limited UK regional funding. This has allowed the stakeholders to form a team and map and understand the individual emission sources – see below17.

What is interesting about this project is that, like in the Rotterdam area, they have managed to bring multiple emitters together to create a decarbonisation and sustainable industrial vision. What this group lacks at present is a store as storage depended on the UK Scottish or UK Southern stores in the now defunct CCS commercialisation process.

Teesside illustrates the potential that can be delivered by a local organisation. If this were expanded into a regional organisation (including the Southern UK and potentially the Scotland region as well) then larger power emitters could be included as could storage.

There is also potential for integration with shipping and the later construction of interconnectors crossing the North Sea joining, for example, the Rotterdam cluster to the UK cluster.

UK Scottish hub

The UK’s main oil province lies in the Central and Northern North Sea off the coast of Scotland. Fifty years of exploration and production mean that the area has well understood and appraised geology, depleted fields and existing infrastructure. The figure to the right shows the oil and gas fields plus the identified saline formations.

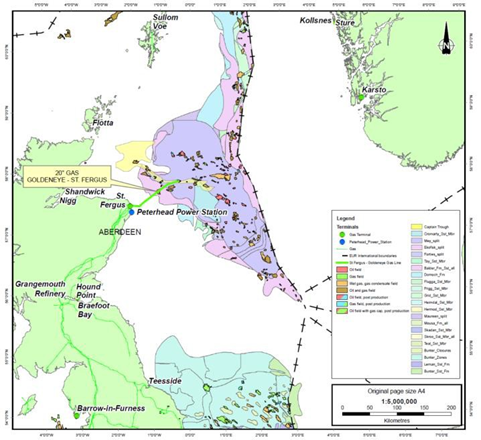

The majority of Scotland’s industrial point- source CO2 emissions (77%, 7.6 Mt in 2014)19 are located around the Firth of Forth, particularly in the Grangemouth area. This area is linked to a gas trunk line that has already been assessed20 for conversion to CO2. This line links the industrial heartland to the St Fergus beachhead of the Goldeneye gas line which joins to the fully appraised Goldeneye21 potential CO2 store.

Although Scottish emissions are modest, the area benefits from the Peterhead deep- water port that is very near the St Fergus pipeline beachhead. The port has been identified as suitable for ship borne CO2 reception. As such the region is a good match to proposals for CO2 collection networks in northern Europe and an export hub at Rotterdam.22

This would allow early expansion, project-by-project, of the first pilot and commercial scale CCS developments in the North Sea Region through access to well-characterised, large capacity storage sites with relatively low capital investment. In turn, in the longer term, when larger CO2 transport volumes become established, new trunk pipelines could sequentially replace shipping routes.

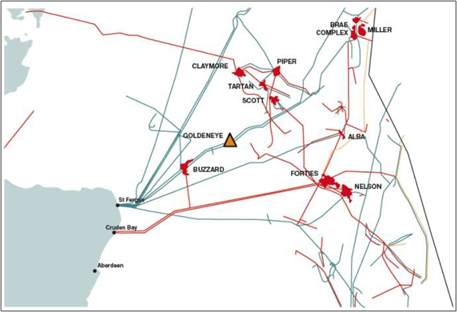

An attraction for the region is the opportunity for CO2 EOR23. Offshore CO2

EOR has the potential to create economic value, extend the productive life of oilfields (e.g. up to fifteen years) with a range of benefits including additional domestic oil revenues, delayed decommissioning, and job retention, as well as providing long-term CO2 storage. Potential EOR candidate fields are illustrated in the figure above24. The combination of geological storage with CO2 EOR has the potential to contribute to the expansion of CO2 storage at low cost. However uncertainty remains in the EOR performance of the fields and significant expenditure is required to retrofit offshore facilities.

Scandinavia Hub

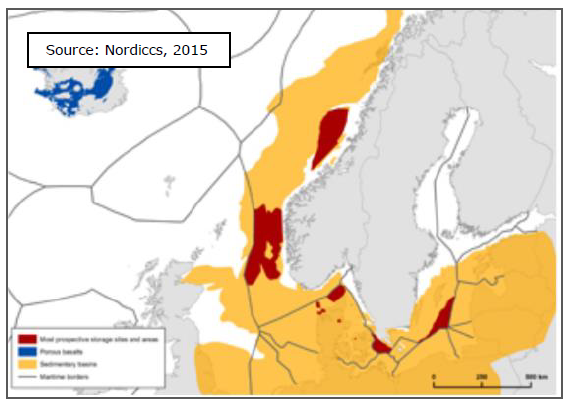

Driven by the development of a Norwegian Industrial CCS Cluster in Southern Norway, this hub is currently being matured through a Norwegian government initiative. Three industrial facilities (cement, fertiliser & waste incineration) are considered for CO2 capture, amounting to between 0.5 and 1.5 million tonnes of CO2 annually. Initial transportation will be by ship to a geological storage facility in the North Sea.

Several concepts on three large potential storage sites are to be evaluated in order to bring forward a transport and storage solution to FID within the next couple of years. This initiative – based on a broad agreement in the Norwegian parliament – aims at implementation of a full-scale CCS value chain from 2020 for a duration of up to 25 years. The initial CO2 volumes injected are expected to characterise and prove geological storage availability for much greater future volumes of CO2 shipped (and later piped) from other Scandinavian sources, including:

Northern Denmark (Aalborg area): up to 7 Mtpa (Europe’s most efficient coal-fired power plant and the largest cement works in Northern Europe)

Western Sweden (Gotenborg area): ca 5 Mtpa (power plant and refinery)

An option for the Scandinavian Hub would be to open up for storage of CO2 from the Baltic region (Luleå, Poland, etc) in North Sea geological storage hubs(s). Once basic infrastructure is in place and magnitude and security of supply of CO2 is established CO2 can also be made available for use in CO2 EOR combined with geological storage.

The storage potential in the Baltic region is unevenly distributed: Denmark, Poland, Germany and Lithuania have considerable storage potential onshore as well as offshore, the limiting factor being regulations and public perception. Finland has no geological storage potential at all, while Sweden has minor potential in the very south. Estonia has suitable geology, but too shallow for storage while Latvia has some deeper lying geology with few storage sites identified. This scarceness of suitable geology could be alleviated by early storage of Baltic CO2 in North Sea storage sites, using ship transportation until local storage options can be developed.

Timing and development path for CCS to contribute to Net Zero

Experience in attempting to develop full chain CCS projects in the UK and the Netherlands has clearly shown that because of the different business cycles in capture, transport and storage, the counter party risk is such that separation of transport and storage into a utility-like business is not only sensible but a necessity. This is expanded on in the ZEP report on Transport and Storage business models and the recent report from the UK Crown Estate25.

Before developing capture projects it is necessary to have a firm guarantee that transport and storage will be available and a clear understanding of the cost. While appraisal can take significant time, over the last decade, a number of EU regions have already invested in early appraisal of CO2 storage. Significant EU funding has also been deployed in exploring the topology of CO2 capture, transport and storage networks26.

Studies, combined with pilot and demonstration projects around the world, have shown that significant decarbonisation is feasible in industry and power.

The regions that have invested in early appraisal share common characteristics:

- they have all identified the strategic opportunity presented by CCS in delivering deep decarbonisation at lowest cost and least disruption to society;

- they have leveraged EU and other sources of funding;

- they have developed or retained organisations that can deploy the relevant competence to inform logical decisions in an impartial manner;

- they have started to develop policies and the financial frameworks that will enable CCS.

Although ZEP would like to see the development and capitalisation of regional Market Makers and construction of storage hubs immediately it appears that the interim step of creating regional development organisations is required. ZEP therefore recommends that the following (initial) organisations be established:

- Nordics – role already potentially filled by Gassnova?

- Central and Northern North Sea – UK

- Baltics

- Eastern Europe onshore

- Iberian peninsula

- Southern North Sea – will encompass industrial regions of Rhine/Ruhr/Rotterdam/Antwerp/Le Havre

These organisations need to be established as soon as politically possible. They will then be able to draw upon the knowledge created by over a decade of EU projects, and local research, to: (i) build the business cases for inward investment, (ii) create the structures required for the establishment of Market Makers and Hubs, (iii) inform the development of focussed capture policies. This will allow regions and Member States to realise the potential for CCS in INDCs by the 2020s and meet the 1.5°C aspiration longer term.

Footnotes

¹ Reference: A CCS future for Europe: catalysing North Sea action. SCCS 2014. Scottish Carbon Capture & Storage. http://www.sccs.org.uk/images/expertise/reports/catalysing/downloads/SCCSConference2014Report.pdf

² Global CCS Institute 2015, The Global Status of CCS: 2015. Special Report: The Role of CCS Hubs and Clusters in Europe, Melbourne, Australia.

³ The UK’s first industrial CCS cluster – introducing the Teesside Collective. Global CCS Institute Insight. Available at: http://www.globalccsinstitute.com/insights/authors/WebinarOrganiser/2015/04/24/uk%E2%80%99s-first-industrial-ccs-cluster-%E2%80%93-introducing-teesside-collective?author=MTc1OTM%3D [Accessed 16 September 2015 with thanks to the GCCSI].

⁴ UK local authority and regional carbon dioxide emissions national statistics. Available at: https://www.gov.uk/government/collections/uk-local-authority-and-regionalcarbon-dioxide-emissions-national-statistics [Accessed 10 September 2015 with thanks to the GCCSI].

⁵ IEAGHG report 2005/2. Building the cost curves for CO₂ storage: European sector http://hub.globalccsinstitute.com/sites/default/files/publications/95736/building-cost-curves-co2-storage-european-sector.pdf

⁶ ZEP. CO₂ Capture and Storage (CCS) in energy-intensive industries http://www.zeroemissionsplatform.eu/library/publication/222-ccsotherind.html

⁷ http://www.eti.co.uk/project/esme/

⁸ ECN have generated a forecast of CO₂ emissions out to 2030; http://www.ecn.nl/docs/library/report/2013/e13019.pdf

⁹ OCAP: Organic Carbon dioxide for Assimilation of Plants.

¹⁰ ROAD: Rotterdam Opslag en Afvang Demonstratieproject.

¹¹ EEPR: European Energy Programme for Recovery.

¹² Previously known as 5/42.

¹³ Bentham M, Mallows T, Lowndes J, Green A (2014) CO₂ Storage Evaluation Database (CO₂ Stored). The UK’s online storage atlas. Energy Procedia, 63, 5103–5113.

¹⁴ Crown Estate.

¹⁵ Industrial regions and climate change policies: Yorkshire and the Humber Regional Report (TUC, 2015).

¹⁶ A blueprint for industrial CCS (Teesside Collective, 2015).

¹⁷ Sarah Tennison (Tees Valley Unlimited) – Teesside Collective: Current Progress on the Industrial CCS Project in Teesside UKCCSRC Cranfield Biannual 21–22 April 2015.

¹⁸ CO₂ Storage Evaluation Database (CO₂ Stored). The UK’s online storage atlas. Bentham, M., Mallows, T., Lowndes, J., and Green, A. Energy Procedia, 2014, 63: 5103–5113. http://www.sciencedirect.com/science/article/pii/S1876610214023558?np=y

¹⁹ Reducing costs of CCS by shared reuse of existing pipeline – case study of a CO₂ capture cluster for industry and power in Scotland. Brownsort, PA., Scott, V., Haszeldine, RS. Article submitted for publication in International Journal for Greenhouse Gas Control, 2016.

²⁰ Assessed as part of the UK Longannet CCS project.

²¹ Assessed as part of the Peterhead CCS project.

²² Overall Supply Chain Optimization. CO₂ Liquid Logistics Shipping Concept. Vermeulen, T. N., 2011. Tebodin Netherlands BV, Vopak, Anthony Veder and GCCSI. Report number: 3112001. http://decarboni.se/sites/default/files/publications/19011/co2-liquid-logistics-shipping-concept-IIsc-overall-supply-chain-optimization.pdf

²³ http://erpuk.org/project/co2-eor/

²⁴ Reference: CO₂ storage and EOR in the North Sea: Securing a low-carbon future for the UK. SCCS, 2015. Scottish Carbon Capture & Storage. http://www.sccs.org.uk/images/expertise/reports/co2-eor-jip/SCCS-CO2-EOR-JIP-Report-SUMMARY.pdf

²⁵ A need unsatisfied: Blueprint for enabling investment in CO₂ storage.

²⁶ Examples include CO2Europipe; The evolution of the extent and the investment requirements of a trans-European CO₂ transport network; ZEP report CO₂ Capture and Storage (CCS) in energy-intensive industries; ZEP report Building a CO₂ transport infrastructure for Europe.

Annex 1: Glossary

| Capex | Capital Expenditure |

| CCS CCS Directive | CO2 Capture and Storage Directive on the geological storage of CO2 |

| CfD | Contract for Difference |

| CO2 | Carbon Dioxide |

| DECOM E&A | Decomissioning Exploration & Appraisal |

| EC | European Commission |

| EEPR EIB EMR | European Energy Programme for Recovery European Investment Bank Electricity Market Reform |

| EOR ETIP | Enhanced Oil Recovery European Technology and Innovation Platform |

| ETS | Emissions Trading Scheme |

| EU | European Union |

| EUA Feasex | Emission Unit Allowance Feasibility Expenditure |

| FID | Final Investment Decision |

| FiT FEED | Feed-in Tariff Front End Engineering Design |

| Mt MS | Mega (million) tonnes Member State |

| NGO | Non-Governmental Organisation |

| O&M | Operation and Maintenance |

| Opex | Operational Expenditure |

| TPA | Third Party Access |

| UK | United Kingdom |

| ZEP | Zero Emissions Platform |

Annex 2: Members of ZEP’s Temporary Taskforce CO2 Transport and Storage

This document has been prepared on behalf of the Advisory Council of the European Technology Platform for Zero Emission Fossil Fuel Power Plants. The information and views contained in this document are the collective view of the Advisory Council and not of individual members, or of the European Commission. Neither the Advisory Council, the European Commission, nor any person acting on their behalf, is responsible for the use that might be made of the information contained in this publication.

* Co-chairs

| Name | Country | Organisation | |

| Shabana | Ahmad | UK | The Crown Estate |

| Tim | Bertels | The Netherlands | Shell |

| Peter | Brownsort | UK | SCCS |

| Niels Peter | Christensen | Norway | Gassnova |

| Benjamin | Court | Belgium | GCCSI |

| Lamberto | Eldering | Norway | Statoil |

| Chris | Gittins | The Netherlands | TAQA |

| Jonas | Halseth | Belgium | Bellona Europe |

| Gardiner | Hill | BP | BP |

| Chris | Littlecott | UK | E3G |

| Philippa | Parminter | UK | SCCS |

| Andy | Read | The Netherlands | ROAD2020 |

| Adam | Richards | UK | National Grid |

| Owain | Tucker* | UK | Shell |

| Keith | Whiriskey* | Belgium | Bellona Europa |