CCU: the potential to reduce CO2 emissions and accelerate CCS deployment in Europe

What is CO2 Capture and Use (CCU)?

The use of captured CO2 as a product (CO2 Capture and Use, or CCU) could be an alternative to – or linked to – the permanent storage of CO2 in geological formations. However, from a climate protection perspective, CCU technologies, which lead to a net reduction in CO2 emissions, should be the main focus, i.e., they ultimately result in products that either show almost no decay over the long term or result in permanent geological storage (CO2 Capture Use and Storage, or CCUS). Mineral carbonation is an example of a natural process that already permanently ‘stores’ CO2.

CCU can also reduce emissions by substituting production methods with alternative, lower-emitting CO2 technologies, e.g., feeding greenhouses with captured CO2 from power plants instead of burning additional natural gas. However, CCU technologies, which result in non-permanent products that are later converted back to CO2 after usage or due to decay within a few decades, may be interesting from an industrial production perspective, but are not relevant for climate protection. Nevertheless, some may act as an enabler or supporter of CCS, thereby having an indirect positive effect, e.g., by strengthening the business case for CCS by creating a product and additional revenues – using a partial CO2-stream.

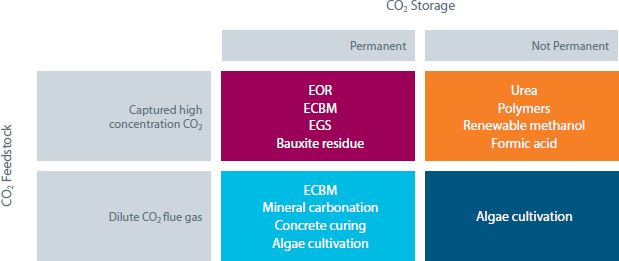

The Global CCS Institute (GCCSI) has identified some CCU technologies in analogous categories:

As CCUS has the highest potential to reduce CO2 emissions, this paper therefore focuses on these technologies, together with those that have the potential to facilitate the deployment of CCS.

CCU must include permanent CO2 storage to qualify as a climate mitigation technology

In order for CCU to qualify as a climate mitigation technology, there must be a long-term storage component. Enhanced Oil/Gas Recovery (EOR/EGR), Enhanced Coal-Bed Methane (ECBM), and mineral carbonation are all technologies that can lead to the permanent storage of CO2. However, in mining activities (e.g., fracking, or as an extraction fluid for oil shales and other unconventional hydrocarbons), the use of CO2 is more concerned with facilitating extraction than permanent storage.

Methods for the tertiary production of oil remaining after primary and secondary recovery are commonly termed EOR. Two such methods – miscible and immiscible flooding – partly or fully rely on CO2 injection. Secondary recovery is based on water injection, but CO2 injection could be promoted as the secondary recovery mechanism.

EOR is by far the most advanced CCUS technology, with decades of experience leading to large-scale, economical operations. In contrast to CCS business models, industrial EOR projects have proven to be economical in cases of cheap CO2 sourcing. With rising oil prices and by combining both business models,

EOR-CCS becomes more attractive and may serve as an important enabler for large-scale CCS. Conservative assumptions estimate an increasing global demand for CO2 for EOR of at least 5%/a, reaching values of 118 Mt CO2 /a (SBS Energy Institute) to 255 Mt CO2 per annum.1

Depleted gas fields also offer significant storage potential. However, increasing and prolonging the tail-end operation of a field via EGR is more strongly limited to specific geological conditions, compared to EOR, and only a few projects exist, e.g., the K12-B offshore operation in the Netherlands. EOR, as well as EGR, leave a considerable share of the CO2 behind in the reservoir, but not necessarily the entire injected volume.

Depending on the geological conditions and operation, the hydrocarbon extraction is accompanied by CO2 release, which may not be accounted for as stored. Monitoring and accounting in accordance with the EU Emissions Trading Scheme (ETS) regulations is therefore key.

Mineral storage is another technology that may be termed CCUS and could, for some industries, be more relevant than storage in the subsurface. Metal oxides (especially alkaline oxides such as CaO and MgO) can react with CO2 to build stable carbonates that may be easily stored or used as materials, mainly in civil engineering. This technological chain leads to a high mass flow with sourcing and logistics challenges in the supply of oxides, while producing a product that may be suitable for the mass market. Alternatively, products of industrial processes (e.g., water purification, ashes) that are already produced at the CO2 emission site may offer mineralisation capacities to bind at least a fraction of the CO2 stream.

CCU could add significant economic value to a CCS project

CCU with only interim fixation of CO2 cannot be seen as CO2 abatement, as the UNFCCC2 has clearly stated. However, adding economic value to a CCS project via a CO2-based product generation could facilitate investments in CCS.

CO2 can be transferred to many different products via chemical, biochemical, photochemical, or electrochemical reactions (DNV 2011). These products may then be used as either feedstock for value-added (bio-)chemicals (e.g., organic and inorganic carbonates, polymers, urea, etc.), or as a medium for intermediate energy storage (e.g., methane, syngas).

Bound in CO2, carbon is in its lowest energetic state for ambient/surface conditions, and any transfer is therefore energy demanding. This plays a role in the economic evaluation, but must also be considered in the energy/CO2 balance of the entire CCU chain. The development of energy-efficient processes, use of excess power, use of renewables (e.g., solar to grow algae), and the advancement of catalysts are therefore of special interest for CCU.

Methanisation and other intermediate energy storage may play an important role in emissions reduction, even if individual projects are neither CO2-abating nor economically feasible as stand-alone projects.

However, by offering energy storage capacities for surpluses generated in electricity, they enable the integration of a higher share of renewables in today’s energy market, thereby reducing the CO2 emissions of the total energy supply system. Their deployment may also benefit from being built upon an existing infrastructure to transport, store, and distribute the products.

CCU should be fully represented in Horizon 2020

ZEP recommends that the following technical gaps, barriers, and topics for further R&D be addressed in the Horizon 2020 roadmap:

- Analyse the market potential of individual CCU technologies.

- Analyse the mitigation potential of CCUS technologies.

- Undertake lifecycle assessments/CO2 balance for CCU technologies.

- Promote the development of CO2-based (mass) products to enable commercialisation.

- Integrate CO2-based energy storage in power-to-gas(-to-power) concepts, including R&D on intermediate or dynamic CO2 storage.

- Reduce the costs of refurbishing oil/gas installations for CO2-EOR.

- Develop smart and flexible offshore solutions to additional equipment requirements, e.g., floating equipment for conditioning, offloading, and re-capture of CO2.

- Establish consistent business models for combining CO2-EOR with CO2 storage and the re-use and storage of a combined stream of CO2 from multiple sources.

- Develop a CO2 supply system for the step-wise development of CCUS, from pilot- to large-scale EOR/EGR, comprising multiple sources and sinks (both petroleum and buffer aquifer reservoirs).

- Combine EOR/EGR with optimised, dedicated long-term storage.

- Develop a flexible design for the CO2-hub, enabling adjustments to local conditions (especially complex for the transport of liquid CO2 by ship).

- Assess operational risks and challenges specific to offshore EOR.

Creating a business case for EOR/EGR with CO2 storage

In the case of CO2-EOR with long-term storage, there are two different drivers (increased oil and CO2 storage), requiring two different business models. In all the 70+ CO2-EOR projects in North America, only the ‘increased oil’ driver is active, with any CO2 storage incidental (even if the CO2 had been anthropogenic, which, in most cases, it is not). The use of captured CO2 for EOR, therefore, unlocks value via increased oil production, but the entire value chain must be in place in order to achieve it. The JRC4 has estimated that annual incremental North Sea oil production in economically viable CO2-EOR/EGR projects could reach 180 million barrels, with the simultaneous storage of 60 million tonnes of CO2.

From an EOR point of view, CO2 is therefore a valuable commodity which should be used sparingly, with ‘losses’ in the reservoir kept at a minimum. CO2 is returned to the surface with the additional produced oil and, after capture, recycled back to the oil recovery activity. Losses in the reservoir depend on local conditions, but generally amount to between 1/3 and 1/5 of the total injected CO2.

Over time, increasing amounts of oil containing CO2 are produced, and the need to add CO2 to the flooding activity decreases correspondingly. For such a CCU project to become a CCUS project, another business plan for maximising CO2 storage is required – driven not by increased oil production, but storage credits. Each link in the chain, therefore, has to make a sufficient return on its investment to have an incentive to start and continue the process, and the work on the business case should focus on potential early movers.

A key driver is the availability of a suitable oil field for EOR, which is affected by factors such as the:

- Maturity of the field, which provides a potential window of opportunity

- Technical suitability of the field

- Strategy of the field owner.

The business case for EGR has the same basic structure as for EOR. However, the revenue per tonne of injected CO2 (on the upstream side) is significantly less as less gas remains from conventional production; the value of the same volume of gas gained per tonne of CO2 is less than for oil; the share of injected CO2 emerging in hydrocarbon production increases more quickly, and early breakthroughs are more likely.

The urgent need for incentives to kick-start CCU projects in Europe

The case for CCS incentives to drive deployment is very clear and will not be further discussed here.5 However, the case for onshore CO2-EOR is not as straightforward, as illustrated by the many projects in the U.S., which were initially set in motion by tax breaks for EOR and not specifically directed at CO2.

In Europe, the greatest potential for CO2-EOR is offshore (mainly in the North Sea) and in Eastern Europe, which has mature fields with historically low recovery rates. Given the costs of offshore EOR, incentives are essential. However, it is critical that they are tailor-made and not confused with incentives for CCS, which could potentially undermine the climate mitigation case and create public mistrust. A similar line of argument would be valid for mineral carbonation storage (and potentially EGR).

Key recommendations

- Develop likely CCUS scenarios for Europe (including on-/offshore CO2-EOR/EGR and CO2 mineral storage) via the European Industrial Initiative on CCS.

- Include CCU and CCUS in Horizon 2020 as an enabling technology for CCS in Europe.

- ZEP to provide recommendations regarding business requirements for successful CCUS in Europe.

- Design tailor-made incentive schemes at the national and EU levels to kick-start early CO2-EOR/EGR and CO2 mineral storage projects (e.g., contributing to the development of logistics structures).

- Urgently resolve transboundary transport, liability, and storage credit allocation issues.