2025: Europe’s carbon management moment? Takeaways from the ICM Summit.

2025 has marked a decisive shift for industrial carbon management: from project development to deployment. With Longship now operational, Northern Lights has begun delivering the first CO₂ injections from industrial sources in Europe. Across the continent, more projects have reached final investment decisions (FIDs) and are under construction, making industrial carbon management a tangible reality.

This progress has been underpinned by growing policy support. Through the Clean Industrial Deal, the EU has recognised industrial carbon management as a key enabler to ensure decarbonisation and competitiveness go hand in hand. Yet, achieving large-scale deployment still requires sustained effort.

It was against this backdrop that the European Industrial Carbon Management Summit took place on 13 October 2025 in Brussels, bringing together more than 250 participants from policymaking, industry, research, and civil society to discuss three key questions: What progress has been made? What remains to be done? What should Europe’s priorities be for 2026?

Let’s look at the key takeaways from this year’s Summit.

Industrial carbon management: A pillar of EU climate policy

2025 was a turning point for industrial carbon management within the EU policy framework.

Building on the Industrial Carbon Management Strategy (2024), the EU began integrating carbon management into the Clean Industrial Deal and the 2040 climate targets.

In a video address, Commissioner Dan Jørgensen reaffirmed the European Commission’s commitment to making carbon management a central element of the Clean Industrial Deal. The updated European Climate Law proposal clearly positions industrial carbon management as a critical tool to achieve the 2040 target.

During a fireside chat, Daniel Mes (EU Competitiveness Taskforce) and Chris Davies (former MEP and Rapporteur of the CCS Directive) highlighted how carbon management supports competitiveness and positions Europe to lead in low-carbon industrial production.

Learning from Europe’s first movers

The Summit showcased lessons from pioneering projects that are paving the way for other initiatives across Europe.

Heidelberg Materials has taken a leading role in making carbon capture a reality for the cement sector. Brevik CCS, the world’s first large-scale carbon capture and storage plant for cement, has been operational since mid-2025. With FID secured for Padeswood CCS, a part of the Hynet Cluster, the company demonstrates that near-zero production is achievable. Heidelberg Materials’ next goal is to replicate this success also in the EU, with six CCS projects supported by the Innovation Fund.

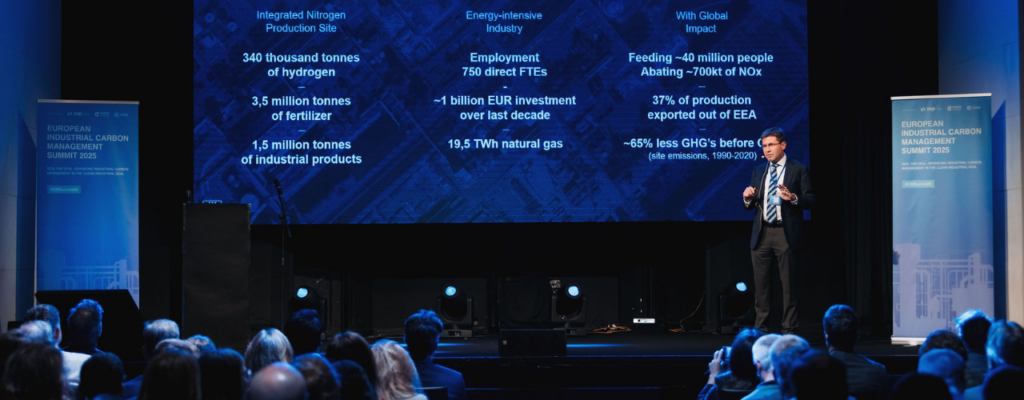

Yara shared progress on its forthcoming CCS project at Europe’s largest fertiliser production site, located in the Netherlands. Operational in 2026, the Sluiskil CCS project will capture up to 800,000 tonnes of CO₂ per year, making it the largest in Europe.

These pioneering examples underline that technology is ready. Now, policy and markets must keep pace.

Building the framework for scale

The coming year will be crucial as the EU finalises implementation of the Net Zero Industry Act (NZIA). The injection capacity obligation under Article 23 of the NZIA, including the setting of penalties, will provide greater clarity to obligated entities.

At the same time, the EU is developing a coherent regulatory framework for the CO₂ market and infrastructure. Legal clarity and a harmonised framework are essential to enable cross-border transport and storage infrastructure and ensure CO₂ capture projects can connect to Europe’s emerging CO₂ network.

The Carbon Removals and Carbon Farming Regulation (CRCF) will also provide pathways for carbon removals to enter compliance markets, establishing a clear framework for permanent carbon removals in Europe.

“We need aggregation of CO₂ sources and an up-and-running CO₂ market in Europe to gain flexibility,” said Luc Haustermans (Yara). He also highlighted the urgent need for a CBAM-export solution: “export for fertilisers is not optional, as our sector supports farmers globally based on seasonal demand.”

Timely delivery will depend on continued political support and commitment, not just by the EU but also by national governments. To support Europe’s first-mover advantage, we need robust policy frameworks – from Carbon Contracts for Difference and CO₂ infrastructure to lead market mechanisms that reward the market uptake of near-zero, carbon-captured materials. Together, these instruments will help build a strong business case for deploying CCS at scale across Europe. – Winston Beck (Heidelberg Materials).

Financing the next wave of projects

While CO₂ capture, transport and storage technologies are technically mature, the major challenge has shifted to commercialising industrial carbon management: ensuring that projects are bankable and scalable across Europe.

Tomás García Moreno (BBVA) noted that CCS projects can reach bankability, as demonstrated by the Northern Endurance Partnership and Net Zero Teesside projects. Klaas Verwer (Equinor) outlined that for large-scale infrastructure developers, the key challenge is aligning timelines between emitters and infrastructure developers to ensure capture projects can commence operations on time.

Ensuring emitters have sufficient financial support to enable capture projects is key to moving forward. In 2026, key policy levers could be unveiled with the advancement of lead markets for low-carbon materials in the Industrial Accelerator Act, the development of an Industrial Decarbonisation Bank and the amendment of the Innovation Fund.

Fertilisers should be among the first lead markets for low-carbon products in the upcoming Industrial Accelerator Act. We need market pull mechanisms for low-carbon products demand and supporting policy frameworks that match the ambition of Europe’s climate goals – Luc Haustermans (Yara)

From proof to scale

2024 was the year Europe placed its bet on industrial carbon management as a priority for a climate-neutral, competitive future. 2025 proved that the bet was well placed, demonstrating that carbon management works in practice. It now stands firmly recognised as fundamental to achieving net zero.

2026 will be the year to scale up. As the EU takes concrete steps to deliver, the hard work will be on ensuring projects receive the infrastructure, funding, and regulatory clarity they need to prosper. The achievements of the first movers will provide the blueprint for the next phase: turning isolated successes into a continent-wide carbon management system.

Authors

Amélie Trémolières is the Communications Manager at ZEP, where she leads the organisation’s communications strategy across institutional communications, policy communications, events, and media relations. She ensures ZEP’s work on climate policy and carbon management technologies is clearly framed, visible, and reaches the right audiences to support ZEP’s objectives.

Before joining ZEP, she worked in several European policy environments, including think tanks such as the Centre for European Policy Studies, government institutions including the French Consulate, and the General Secretariat of the Council of the EU as a digital communications trainee. She also spent two years as Communications and Events Operations Lead at a Brussels-based European association.

She has expertise in media relations, social media strategy, website management, and branding. Amélie holds an academic background in EU studies and political and public communication, is a native French speaker, and has a strong interest in climate and EU policy.

Iria supports ZEP’s work by building and strengthening relationships with partners, supporting the organisation’s membership community, and fostering collaboration and engagement across stakeholders within the ZEP ecosystem.

Before joining ZEP, Iria worked as a Project Manager in POLITICO Europe’s Live division. She has also supported Flanders Investment & Trade and worked in consultancy. She has a background in law and global governance, with further studies in global management and economic diplomacy.

Outside of work, Iria enjoys live music, learning new languages, discovering under-the-radar coffee spots around the city, staying up to date with current affairs, and spending time with friends and family.